Reflecting the global nature of the financial malaise and its associated uncertainty, growth rates in most advanced countries have slowed in the second quarter. The slowdown may have triggered a global banking crisis.

More specifically, the U.S. GDP grew at a sluggish 1.2 percent rate in the second quarter as businesses continued to hold back on investments. Given a downward revision of the growth by the US Commerce Department to just 0.8 percent in the first quarter as compared to 1.1 percent that was previously estimated, the average growth rate for the first half of this year is just 1 percent. The US GDP growth for three consecutive quarters has been hovering close to 1 per cent.

|

| The US GDP Quarterly Growth Rate |

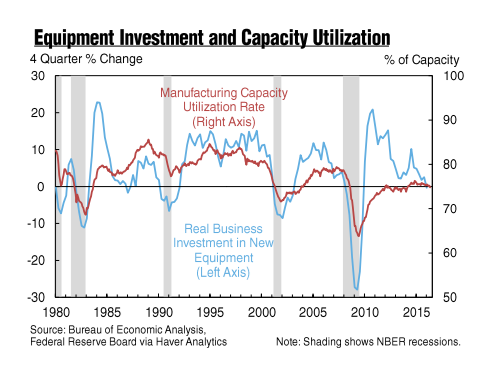

This slow growth pattern should not be a surprise to the readers of this blog as we have persistently warned about the implications of businesses adoption of the intensive margin mode of production and delays in investing for capital formation arising from the prevailing uncertainty. The fact that in the US widespread slow growth in the second quarter was stemming from a fall in inventories, at a time when personal consumption was growing at 4.2 percent, has validated our hypothesis. Moreover, for the third consecutive quarter, nonresidential business investment in the US declined in the second quarter by 2.2 percent, indicating that businesses are refraining from the irreversible capital expenditures. The situation is not much different in the rest of the advanced countries.

In Japan, a ¥28 trillion ($273 billion) in new spending, announced in the early August, as part of the Second Arrow of Abenomics, meaning fiscal stimulus, to jump-start the Japan's sluggish economy is not expected to alter the global distortion of fundamentals. Precisely because of the uncertainty, Japan's $130 billion dollars worth of new fiscal stimulus, including cash payouts to low-income earners and increased infrastructure spending, earmarked for upgrading port facilities for cruise ships, as well as accelerated construction of a high-speed train line, is not expected to create much of incentives for capital formation in the country's export-oriented industrial sector. The only solution, as we have repeatedly called for in this forum, is a global accord to restructure the toxic debts and to realign various currencies based on the real purchasing power parity.

Unfortunately, the illusory appearance of a strong US labour market, with her unemployment rate at 4.9 percent, may have disguised the severity of the problem. The quasi-strength, however, is mainly due to the use of contingent labour in the intensive-margin capacity planning of businesses where firms substitute labour for capital due to uncertainty. This is exactly why wage growth has remained anemic. The slowing of global growth is setting into motion a vicious circle that could, with an increasing probability, trigger a global banking crisis.

As the following charts show European banks' shares have already plummeted to some distress levels as they are saddled with $1.3 trillion in non-performing loans, nearly $400 billion of them in Italy, and many don’t have sufficient capital buffer. The situation will dramatically worsen if the current slowdown develops into a highly probable global recession.

|

| Barclays PLC |

|

| Royal Bank of Scotland Group |

|

| Deutsche Bank AG |

|

| Banco Santander SA |

|

| Monte dei Paschi di Siena |

In spite of its convoluted narrative, the IMF's latest Global Financial Stability Report acknowledges that for many European banks, elevated non-performing loans comprise a major structural weakness. According to the report roughly one-third of listed European banks (by assets) are facing significant challenges to attaining sustainable profitability arising from legacy issues (900 billion of non-performing loans and an unspecified amount of toxic assets).

Deteriorating profitability and unresolved legacy challenges raise the risk that external capital and funding could become more expensive, particularly for weaker banks with very low equity valuations (price-to-tangible-book valuations of less than 60 percent), pointing to weak future prospects. Italian banks face a particular challenge in this regard, as market pricing has reflected investor concerns that some banks may face difficulties in growing out of their substantial NPL overhang, despite constructive steps taken by Italian authorities to facilitate balance sheet repair.

Italy, like other eurozone's weaker economies, including Greece, Portugal, and Spain that have been severely afflicted by the Big Recession, most probably will experience acute distress and becomes the first major country fully exposed to the brunt of this vicious circle. During the six consecutive years of recession since 2007, Italy's GDP has declined by 10 per cent and the country's banks, that rely heavily on retail deposits and bonds to finance their lending, have accumulated about €400bn of non-performing loans, compromising more than 18 percent of their total loans.

The EBA tests did not include any banks from Greece or Portugal, . The two Irish banks, AIB and Bank of Ireland were among the worst financial institutions.The results will have adverse impact on plans to starting selling down the Irish government's stake in AIB next year. In the words of Philip Lane, Ireland's Central Bank governor: the two banks

are adequately capitalised but remain vulnerable to a downturn, especially in relation to the continued workout of problem loans and the sustainability under stress of current profitability levels.”

The Italian banks are already exhibiting the first signs of stress and with their eminent insolvency a global contagion of banks' failure would be inevitable. For instance, according to the recent EBA stress test, the oldest operating bank in the world: Monte dei Paschi di SienaBanca was the worst performing bank among the 51 participating banks in the test, requiring to raise massive amount of capital. The bank would be insolvent inthe European Banking Authority(EBA)'s stress test that was released on July 29th, with a common equity tier one (CET1) ratio of -2.44 per cent. Banks are central to the European financial system, supplying about three quarters of all credit, and their demise therefore will be a devastating blow to the economy in Europe.

The bail-in solution for banks on the verge of insolvency, suggested by the newly established EU’s banking union, that has become operative earlier this year, requires that the bank's shareholders , creditors and large depositors (i.e., in excess of €100,000) to assume a haircut before taxpayers' funds can be used to bail them out. Bondholders, of course dislike "bail-in" remedies, and many are concerned about the inconsistent and at times chaotic bail-in procedures that are adopted in trying to prevent bank failures. These policies have increased the risk of funding for smaller lenders. Moreover, the looming prospect of bail-in has diminished the supply of credit for the smaller lenders that are mainly concentrated in the weaker economies, exacerbating the banking challenges.

For instance, when the Italian government in 2015 decided to bail-in junior, or subordinated, bondholders at four small insolvent regional banks it generated a significant hardship for retail investors and pensioners because many of the banks’ junior bonds had been sold to them as riskless savings products. The move also frightened the investors.

To guard against a bail-in the board ofMonte dei Paschi di Sienahas approved a conditional recapitalization of the bank, guaranteed by a consortium of investment banks led by J.P. Morgan Chase. Nevertheless, the bank's prospects remain gloomy, particularly in the event of a global recession.

|

| Impact on Common Equity Tier 1 (CET1) capital ratio from 2015 to 2018 in the adverse scenario by bank in alphabetical order. Source: EBA |

|

| Evolution of absolute credit losses (€ bn) and contribution of cumulative credit risk losses in the adverse scenario for selected countries of the counterparty (%). Source EBA |

According to a study byAcharya, Pierret and Steffen, to meet the robustness standards specified by the U.S. Federal Reserve, Europe’s largest banks, including HSBC Holdings PLC, Deutsche Bank AG and UniCredit SpA, would need to raise more than €253 billion in capital rising to more than €572 billion in a crisis situation. The study focusing on 34 of the largest European banks, with more than €23 trillion in assets, also found they would need to raise more than €1.19 trillion, potentially from governments, to have enough equity to withstand another financial crisis. According to the study:

A. French banks lead almost each book and market capital shortfall measure, both in absolute euro amounts and relative to its GDP. The capital shortfall ranges from €2 billion to €189 billion. The Capital Shortfall in a Systemic Crisis stress scenario (SRISK) suggests a shortfall of €248 billion, which corresponds to almost 12% of the country’s GDPNotwithstanding these discouraging numbers, the results of EBA's stress test suggest that only a handful of banks will be facing the challenge of maintaining sufficient capital in the event of a hypothetical severe economic downturn. As a matter of fact, however, should a contagion scenario come to pass even the Acharya et al results would be too optimistic. The severity of European debts, anemic global growth, negative interest rates, currency wars, and a rapidly deteriorating international trade's outlook render the EBA results even-more questionable.

B. The banks with the largest SRISK next to France are from the U.K., Spain and Germany. While German banks benefit from a stronger domestic economy with a higher GDP and capacity for public backstops, shortfalls relative to the GDP of these countries is large corresponding to almost 11% in Spain and 7% in the U.K.

C. Italian banks have capital shortfalls of €97 billion, which correspond to about 6% of Italy’s GDP.

The world urgently needs a global financial accord to cleanse the system of its toxic assets, realign currencies, and reestablish trade links.