On Wednesday 19th December , the Federal Reserve announced its 25 basis-point rate hike. The Dow Jones industrial average and other major indexes tumbled , and this was perhaps the reason why some of my students wrote me to ask for an update on my July note, in which I had stated:

To be sure, the Fed has been under scrutiny in recent months for its efforts to normalize monetary policy. It had kept its benchmark interest rate anchored near zero for seven years, and in numerous occasions, in these notes, we have discussed the futility and the risks of the QEs which have been exacerbating the global imbalances. We have argued for a new global financial order based on a meaningful restructuring of global debts, and a fundamental rebalancing of the global imbalances. Of course, we have been aware that the Quantitative Easing policies (QEs) had provided some artificial support for the stock market, keeping it aloft, and we have been expecting that with the onset of Quantitative Tightening policies (QTs) we would be seeing some opposite effects. However, these effects would pale in comparisons with the dramatic correction to be expected in response to a rapidly deteriorating structural imbalances, associated with high levels of governments and corporations debts, inflated central banks balance sheets, and trade conflicts.

It would be a misguided argument, drawn from a conventional stabilization policy analysis, to maintain that a correctly formulated set of QTs could somehow prevent the danger of the upcoming financial crisis. We have argued that the impacts of conventional stabilization policies, including the unorthodox QEs and QTs in a disequilibrium context, in which the equilibrium conditions in virtually all markets have been highly distorted, are not easily quantifiable. We have argued that the conventional methodology for calculating the output gap would be misleading in the current situation in which, due to the prevailing uncertainties, firms investment strategies are focused on the utilization of contingent labour and contingent capital.

Unfortunately, the appearances, from time to time of, quasi- equilibrium conditions, which have been local and highly unstable, have been misinterpreted by many analysts, including the policy makers, as the long-term global equilibrium. Although such short-term equilibria, arising from agents' optimizations, under obstreperous QEs, had provided the illusive dynamics of a healthy growth, with the associated increase in employment and consumer confidence, in reality they were based on highly unstable supply and demand functions. Expectations of a soft-landing, in such a flimsy circumstances are a wishful thinking that always, and to a large extent, aggravate the severity of a crash.

The Fed rate hike came in a background of softening global growth, relatively low inflation and volatile stock market, with the monetary authority expecting two more rate hikes in 2019, as compared to their previous forward guidance of three increases next year. Also, the Fed statement sounded slightly more nervous, as it did not include the qualifier 'some' in its previous statement, stating:

Some analysts were quick to blame President Trump for this sorry state of affairs. According to CNBC;

The problem is that with the imminent appearance of a severe recession the policy makers may decide to resort to another round of QE, which unfortunately would be even more ineffective than the previous rounds. Furthermore, with the federal funds rate target at a range of 2.25 percent to 2.5 percent, the Fed will not simply have enough ammunition for an effective interest rate response. The fact is that the discussion about the level of neutral rate at this juncture is a red herring. Nobody can predict the new long-term equilibrium conditions before the cleansing of all excesses.

Economic growth, has already exhibits a decline from its 4.2 percent rise in the second quarter, and it is clear that it will be slowing dramatically in 2019, as not only the impacts of artificial boosters such as tax cuts and spending increases wanes, but more seriously as the global uncertainty that is flared up already, triggered by Brexit, European financial situation, debt overhang in China, massive global corporate debt and the trade war exerts its impact. These impacts could be magnified by the rise of artificial intelligence-driven electronic trading as it accelerates financial transactions, allowing them to be conducted across multiple markets at the same time. Thus, a possibility of an emerging sudden deflationary dynamics cannot be ruled out.

The European Saga

According to the European Financial Stability Review, November 2018;

Under this relatively optimistic scenario, British lenders would be able to withstand a global recession more severe than a disorderly Brexit. The test indicates that British banks would be able to keep lending to customers even if there were a major financial crisis, while continuing to pay billions of pounds in fines and compensation to address wrongdoing. “The test shows the UK banking system is resilient to deep simultaneous recessions in the UK and global economies that are more severe overall than the [2008] global financial crisis,” the BoE wrote in the introduction to the stress test results. Despite, the fact that the results appear to have been presented to appease the bickering Brexiteer politicians, still the Bank's efforts are more encouraging than those of the Fed, which perhaps being worry of provoking President Trump's wrath has been resistant to conduct broad-based, macro stress tests on its systemically important financial institutions (sifis).

Some central bankers are more vocal with regard to their concerns about the upcoming financial crisis. For instance, Bank of France governor Francois Villeroy de Galhau has stated: “To measure the global impact of shocks, we need in particular to have macro stress tests of liquidity, including for investment funds." In France, where national debt is set to hit 98.7 percent of GDP in 2018, president Macron, who thought pursuing a Gerhard Schröder's type of more business-friendly reforms, would be improving its long-run growth potential suddenly faced with the so-called ‘yellow vest’ protests. Outraged by his wage and welfare reducing policies, under a highly skewed distribution of income in favour of rich, Gilet June protesters torched cars, attacked shop windows and clashed with police. The president was forced to deliver a much-watched mea culpa in mid-December to mollify protestors, and offered a handful of concessions; raising the minimum wage and slashing some taxes that would push next year’s fiscal deficit well beyond the EU-mandated threshold of 3.0% of GDP. The French government has warned of slower economic growth as a result of the protests and Bruno Le Maire, the country's finance minister, has stated that the current protests would cost France 0.1 percentage point of quarterly economic growth. France growth rate was a meager 0.4 percent in the third quarter from the previous quarter.

With large French and German banks owning billions of Italian sovereign debt, including BNP Paribas €9.8 billion, BPCE €8.5 billion and Crédit Agricole €7.6 billion, at the end of 2017, the chronic financial problems of Italy is the prime trigger for a financial crisis that could spread across the EU. These problems include Italy's huge accumulation of nonperforming loans on its banks’ balance sheets, amidst of the efforts by its populist government to spend money, that it doesn’t have, to improve the country's long lasting lethargic growth Rome's debt is more than €2 trillion and 131 percent of its GDP, the second highest in the EU after Greece.

And Finally China's Slowdown

In China a weaker credit growth, slowing global demand and higher U.S. tariffs on Chinese shipments are affecting its investment and export prospects, and thus its GDP. Her GDP growth slowed to 6.5 percent in the third quarter, the weakest pace since the global financial crisis, and with the recent data showing softness in November factory output and retail sales, it is quite clear that the economy is already slowing down. China's official Purchasing Managers' Index (PMI) fell to 50, from its previous level of 50.2. A reading below 50 indicates that an economy is contracting. The last time China saw a no-growth headline figure was in July 2016:

China's domestic economic imbalances are serious. The country's regional banks are heavily incentivized to keep loss-making companies alive. To avoid the appearance of loan losses, the banks extend loans to zombie firms, allowing them , in the short term, to maintain an illusion of profitability. The asset quality of many banks are quite poor, and they rely heavily on interbank borrowing as source of funding, which can dry up fast when it is most needed during a financial crisis. For instance, according to data from 244 Chinese lenders, the share of deposits in total liabilities at regional banks fell from 73 per cent to 64 per cent between 2013 and 2017. Once banks levering up through non-deposit sources, the cost of funds increases and the odds for an interest rate shock or a liquidity shock rise substantially.

The country's debt levels are soaring from 140 percent of GDP in 2008 to more than 260 per cent now. Despite four reductions to banks' reserve requirements, tax cuts and increased construction spending, lending remains tight and money supply now sits near record lows.

[B]ased on some theoretical guesses, the probability of a sharp economic slowdown has increased by an order of magnitude. There are reasons to believe that the short-term aggregate supply curve and the long term potential have began to shift to the right, while because of "borrowing from the future" and large budget deficit the aggregate demand will shift to the left. The result would be the onset of recessionary forces that their amplitude could be wider than the previous one in 2008-09.I have to confess that last February, against his advice I told my broker that I do want to get out of equities, and as stock markets were rising again, for couple of months I had to bear with his grumbling noises about my unwise decision. In this note I am about to reiterate my argument that we are going to see a major and frightening correction of Dow, to a level perhaps around 14000, that would augur the emergence of another financial crisis. It goes without saying that the economy may go sideways and we may be dealing with an stagnating market until 2026, and perhaps beyond. Obviously some short term reversals of the recent declines are to be expected, since as the saying goes even a dead cat will bounce when it's dropped from a towering height.

|

| Dow Jones - 10 Year Daily Chart |

To be sure, the Fed has been under scrutiny in recent months for its efforts to normalize monetary policy. It had kept its benchmark interest rate anchored near zero for seven years, and in numerous occasions, in these notes, we have discussed the futility and the risks of the QEs which have been exacerbating the global imbalances. We have argued for a new global financial order based on a meaningful restructuring of global debts, and a fundamental rebalancing of the global imbalances. Of course, we have been aware that the Quantitative Easing policies (QEs) had provided some artificial support for the stock market, keeping it aloft, and we have been expecting that with the onset of Quantitative Tightening policies (QTs) we would be seeing some opposite effects. However, these effects would pale in comparisons with the dramatic correction to be expected in response to a rapidly deteriorating structural imbalances, associated with high levels of governments and corporations debts, inflated central banks balance sheets, and trade conflicts.

It would be a misguided argument, drawn from a conventional stabilization policy analysis, to maintain that a correctly formulated set of QTs could somehow prevent the danger of the upcoming financial crisis. We have argued that the impacts of conventional stabilization policies, including the unorthodox QEs and QTs in a disequilibrium context, in which the equilibrium conditions in virtually all markets have been highly distorted, are not easily quantifiable. We have argued that the conventional methodology for calculating the output gap would be misleading in the current situation in which, due to the prevailing uncertainties, firms investment strategies are focused on the utilization of contingent labour and contingent capital.

Unfortunately, the appearances, from time to time of, quasi- equilibrium conditions, which have been local and highly unstable, have been misinterpreted by many analysts, including the policy makers, as the long-term global equilibrium. Although such short-term equilibria, arising from agents' optimizations, under obstreperous QEs, had provided the illusive dynamics of a healthy growth, with the associated increase in employment and consumer confidence, in reality they were based on highly unstable supply and demand functions. Expectations of a soft-landing, in such a flimsy circumstances are a wishful thinking that always, and to a large extent, aggravate the severity of a crash.

The Fed rate hike came in a background of softening global growth, relatively low inflation and volatile stock market, with the monetary authority expecting two more rate hikes in 2019, as compared to their previous forward guidance of three increases next year. Also, the Fed statement sounded slightly more nervous, as it did not include the qualifier 'some' in its previous statement, stating:

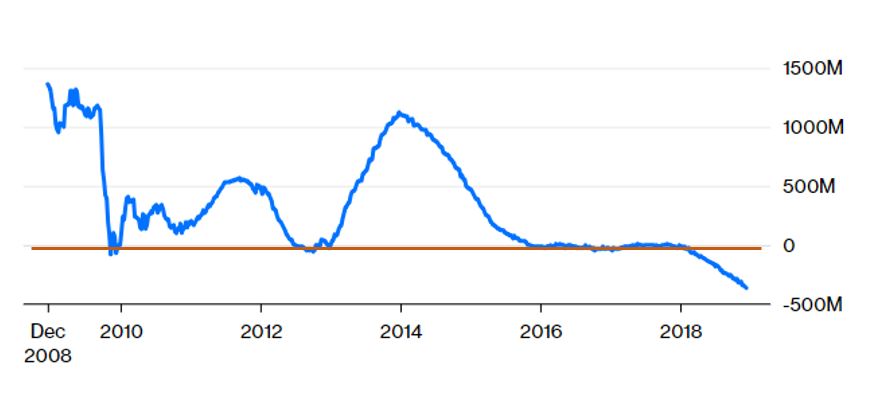

“The Committee judges that some further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective over the medium term.”Moreover, Chairman Jerome Powell said that he would keep reducing Fed's balance sheet by up to $50 billion per month. It should be noted that since the beginning of the QT process in October 2017, the Fed has trimmed its dangerously inflated balance sheet by a meager $365 billion to $4.14 trillion, relative to what is really needed, which is a virtually impossible to attain reduction of some $3 trillion. According to the chairman:

“We thought carefully about how to normalize policy and came to the view that we would effectively have the balance sheet runoff on automatic pilot and use monetary policy, rate policy to adjust to incoming data. I think that has been a good decision,”

|

| Total Assets of the Federal Reserve ($million) |

|

| Year-on-year change in the Federal Reserve balance sheet ($000) |

The end of 2018 makes clearer every day that the president himself represents a fundamental problem for America's economy and national security alike. Trump's erratic behavior and weak leadership have unsettled Wall Street and Washington alike — and there's every reason to expect things will get worse. :While, I am not certainly a fan of president Trump's shenanigans and at times his irrational behaviour, nevertheless, I find this kind of accusation bordering to nothing more than a cheapshot. On the other hand it is hard to understand Treasury Secretary Steven Mnuchin's declaration on the weekend of December 22, that markets have enough liquidity for lending. Yes, it is true that according to Goldman and Sachs data the large Banks have now 39% more liquidity as compared to 2010, and the comparative rates for trust banks and regional banks in the US are 73% and 71% respectively. However, in a world with close to $1.3 quadrillion of financial debt instruments, including derivatives, and a global GDP of close to $90 trillion these percentages would be meaningless, particularly in the event of a major financial crisis, when the Fed balance sheet has increased close to 500 percent, and the US public debt has increased by about 63% over this time span.

The problem is that with the imminent appearance of a severe recession the policy makers may decide to resort to another round of QE, which unfortunately would be even more ineffective than the previous rounds. Furthermore, with the federal funds rate target at a range of 2.25 percent to 2.5 percent, the Fed will not simply have enough ammunition for an effective interest rate response. The fact is that the discussion about the level of neutral rate at this juncture is a red herring. Nobody can predict the new long-term equilibrium conditions before the cleansing of all excesses.

Economic growth, has already exhibits a decline from its 4.2 percent rise in the second quarter, and it is clear that it will be slowing dramatically in 2019, as not only the impacts of artificial boosters such as tax cuts and spending increases wanes, but more seriously as the global uncertainty that is flared up already, triggered by Brexit, European financial situation, debt overhang in China, massive global corporate debt and the trade war exerts its impact. These impacts could be magnified by the rise of artificial intelligence-driven electronic trading as it accelerates financial transactions, allowing them to be conducted across multiple markets at the same time. Thus, a possibility of an emerging sudden deflationary dynamics cannot be ruled out.

The European Saga

According to the European Financial Stability Review, November 2018;

The euro area financial stability environment has become more challenging since the publication of the previous Financial Stability Review in May. On the positive side, a growing economy and improved banking sector resilience have continued to support the financial stability environment in the euro area.As for the Brexit, the Bank of England has already warned Britain would be tipped into a recession worse than the financial crisis in the event of a no-deal disorderly Brexit. The Bank's analysis of various EU withdrawal scenarios, shows that in the event of a disorderly Brexit, Britain's GDP could fall by 8%. The Bank of England has also investigated the impact of an stress scenario on the British financial institutions. The scenario assumes, gross domestic product would fall by 4.7 per cent in the UK and 2.4 per cent worldwide, while residential property prices in the UK would fall by a third and the BoE’s base rate would rise to 4 per cent.

Under this relatively optimistic scenario, British lenders would be able to withstand a global recession more severe than a disorderly Brexit. The test indicates that British banks would be able to keep lending to customers even if there were a major financial crisis, while continuing to pay billions of pounds in fines and compensation to address wrongdoing. “The test shows the UK banking system is resilient to deep simultaneous recessions in the UK and global economies that are more severe overall than the [2008] global financial crisis,” the BoE wrote in the introduction to the stress test results. Despite, the fact that the results appear to have been presented to appease the bickering Brexiteer politicians, still the Bank's efforts are more encouraging than those of the Fed, which perhaps being worry of provoking President Trump's wrath has been resistant to conduct broad-based, macro stress tests on its systemically important financial institutions (sifis).

Some central bankers are more vocal with regard to their concerns about the upcoming financial crisis. For instance, Bank of France governor Francois Villeroy de Galhau has stated: “To measure the global impact of shocks, we need in particular to have macro stress tests of liquidity, including for investment funds." In France, where national debt is set to hit 98.7 percent of GDP in 2018, president Macron, who thought pursuing a Gerhard Schröder's type of more business-friendly reforms, would be improving its long-run growth potential suddenly faced with the so-called ‘yellow vest’ protests. Outraged by his wage and welfare reducing policies, under a highly skewed distribution of income in favour of rich, Gilet June protesters torched cars, attacked shop windows and clashed with police. The president was forced to deliver a much-watched mea culpa in mid-December to mollify protestors, and offered a handful of concessions; raising the minimum wage and slashing some taxes that would push next year’s fiscal deficit well beyond the EU-mandated threshold of 3.0% of GDP. The French government has warned of slower economic growth as a result of the protests and Bruno Le Maire, the country's finance minister, has stated that the current protests would cost France 0.1 percentage point of quarterly economic growth. France growth rate was a meager 0.4 percent in the third quarter from the previous quarter.

With large French and German banks owning billions of Italian sovereign debt, including BNP Paribas €9.8 billion, BPCE €8.5 billion and Crédit Agricole €7.6 billion, at the end of 2017, the chronic financial problems of Italy is the prime trigger for a financial crisis that could spread across the EU. These problems include Italy's huge accumulation of nonperforming loans on its banks’ balance sheets, amidst of the efforts by its populist government to spend money, that it doesn’t have, to improve the country's long lasting lethargic growth Rome's debt is more than €2 trillion and 131 percent of its GDP, the second highest in the EU after Greece.

And Finally China's Slowdown

In China a weaker credit growth, slowing global demand and higher U.S. tariffs on Chinese shipments are affecting its investment and export prospects, and thus its GDP. Her GDP growth slowed to 6.5 percent in the third quarter, the weakest pace since the global financial crisis, and with the recent data showing softness in November factory output and retail sales, it is quite clear that the economy is already slowing down. China's official Purchasing Managers' Index (PMI) fell to 50, from its previous level of 50.2. A reading below 50 indicates that an economy is contracting. The last time China saw a no-growth headline figure was in July 2016:

China's domestic economic imbalances are serious. The country's regional banks are heavily incentivized to keep loss-making companies alive. To avoid the appearance of loan losses, the banks extend loans to zombie firms, allowing them , in the short term, to maintain an illusion of profitability. The asset quality of many banks are quite poor, and they rely heavily on interbank borrowing as source of funding, which can dry up fast when it is most needed during a financial crisis. For instance, according to data from 244 Chinese lenders, the share of deposits in total liabilities at regional banks fell from 73 per cent to 64 per cent between 2013 and 2017. Once banks levering up through non-deposit sources, the cost of funds increases and the odds for an interest rate shock or a liquidity shock rise substantially.

The country's debt levels are soaring from 140 percent of GDP in 2008 to more than 260 per cent now. Despite four reductions to banks' reserve requirements, tax cuts and increased construction spending, lending remains tight and money supply now sits near record lows.