Monetary authorities around the world are busily introducing ineffective policies that they hope would create growth. As a result the state of the global economy increasingly looks like approaching the instant when Wile E Coyote runs off a cliff, but keeps spinning his legs, unaware that an impending hard landing is practically unavoidable. Actually, the unresponsive world economy can be represented by yet another illustrative allegory, the movie Weekend at Bernie's, where two financial professionals (a metaphor for the central bankers), who have discovered a large insurance fraud scam in their company (a metaphor for Too Big to Fail, QEs, or negative interest rates, etc.), are invited to a party at their boss’s beach house over Labor Day. Only when they get there, they discover that their boss Bernie (the global economy) is dead from what looks like a drug-overdose (the massive $225 trillion of debt, and $600 trillion of toxic assets.) Instead of doing the right thing the two executives decide it better to pretend he’s still alive so they can keep partying!

Like the young executives in Weekend at Bernie's central

bankers around the world have been increasingly using unconventional policies to

prop up the global economy, expecting to convince investors that their policies

are working and hoping nobody would notice all the Bernie's vital signs have been extinguished,

i.e., the transmission mechanism of monetary policy is shattered . The world’s largest

four central banks bought assets worth $1.2 trillion in 2015, similar to the

amounts purchased post-Lehman and during the 2013 euro-area crisis, with a very

little impact on growth. Meanwhile, they are futilely waiting for cheaper oil impacts

come to rescue and give a boost to the world economy. The fact that growth has not yet accelerated

after the collapse of oil prices is blamed on the lag structure of impacts and

not on the prevailing global uncertainty about the outlook that has weighed

seriously on financial markets.

Negative Interest Rates, and market Volatility

Both the Bank of Japan and the European Central Bank cut

rates further into negative territory this year, and both saw their currencies

strengthen. This is largely because markets has started to realize that these

prop ups are not able to revitalize the economy. Particularly, when in the

words of Governor Carney in his G20 speech in Shanghai

“Volatility has spilled over into corporate bond markets with US high-yield spreads at levels last seen during the euro-area crisis. The default rate implied by the US high-yield CDX index is more than double its long-run average. And sterling and US dollar investment grade corporate bond spreads are more than 75bp higher over the past year. "That volatility has not disappeared, it will show up soon with Brexit referendum and in the meanwhile, after the latest Fed’s move, is morphed into more of exchange rate volatility.

Business Fixed Investment, and Intensive Margin

While, the FOMC statement in March reported that economic activity has been expanding at a moderate pace despite the global economic and financial developments of recent months, it also noted that business fixed investment and net exports have been soft. Undeniably, the strong US job gains in the absence of strong fixed investment, contrary to Fed’s reading, cannot point to additional strengthening of the labor market. As we have repeatedly argued in the past the strong job gains have been mostly emanating from a greater business focus on intensive margin due to the prevailing uncertainty. An intensive margin implies that instead of investing on latest technology firms hire more labour and utilize their existing equipment capacity more intensely. The substitution of transitory labour intensive tactics ( such as introduction of extra production shifts for part-time workers) instead of committing to irreversible longer-term fixed-capital investment has been the main reason for increased use of contingent employment and weak wage growth.

While, the FOMC statement in March reported that economic activity has been expanding at a moderate pace despite the global economic and financial developments of recent months, it also noted that business fixed investment and net exports have been soft. Undeniably, the strong US job gains in the absence of strong fixed investment, contrary to Fed’s reading, cannot point to additional strengthening of the labor market. As we have repeatedly argued in the past the strong job gains have been mostly emanating from a greater business focus on intensive margin due to the prevailing uncertainty. An intensive margin implies that instead of investing on latest technology firms hire more labour and utilize their existing equipment capacity more intensely. The substitution of transitory labour intensive tactics ( such as introduction of extra production shifts for part-time workers) instead of committing to irreversible longer-term fixed-capital investment has been the main reason for increased use of contingent employment and weak wage growth.

By the mid-March, the experience of five consecutive weekly

gain for various stock indexes including the Dow, S&P and Nasdaq created

the impression that the recent weakness in markets is over. Recall that the weakness has been observed since the Fed’s

December interest rate rise. Many market analysts were excited that an

estimated loss of more than 6 trillion dollars since early January has been recovered, and reported that their earlier concerns about slowing global growth is now waning

and the outlook for commodity prices has improved. Nobody, mentioned any fundamental factors. Some

attributed the recovery to a rather sharp rise in oil prices and expectations

of higher US growth, despite the global slowdown.

High Debt, Banks' Non-performing Loans, and Shanghai's Accord

Yet these factors pale in significance when viewed against global debt, including the U.S. gross national debt that according to some estimates would reach a level of $24 trillion by 2020, or just over 100% of gross domestic

product, which can surge to $27 trillion if Mr. Trump’s tax cuts are

implemented, assuming, of course, that the global economy withstands the

shock to international trade stemming from his anti-trade rhetoric. Similarly

European sovereign and private debts are quite high while banks’ non-performing

loans are disturbingly rising. These are fundamental factors which would not allow a

return to a smooth normal growth path – even if policymakers are content with a

slow growth trajectory. Wile E Coyote has now reached the edge of debt and QEs

cliff.

Given the urgency of the moment, many of us expected that

the G20’s February 25th meeting in Shanghai would come up with some fundamental

agreement to rebalance the global economy, would try to readjust values of various currencies by employing some version of Purchasing Power Parity, and would restructure debts. It was hoped that such policies would rescue the banking

sector before a full blown financial crisis set in. Regrettably, once again the International

Monetary Fund (IMF) did come up with an entirely inappropriate policy

recommendation and instead of arguing for resolving the global financial

imbalances, a restructuring of global debts, and an end to currency wars,

argued for a coordinated stimulus program! Fortunately, it was soundly

rebuffed by both Germany and the United States.

Nevertheless, the

flurry of erratic monetary policy announcements after the Shanghai meeting has

led some to conclude that there must have been a secret Plaza type Accord in Shanghai

to adjust exchange rates and create some semblance of truce in the currency wars.

However, for that hypothetical accord to be successful the necessary conditions

are transparency and completeness, neither of which exist. In other words the accord must deal with the astronomical

global debt, and must provide a framework for the orderly currency readjustments. All

in all, though, judging from the inconsistency of various monetary policies it appears

that a putative Shanghai accord, even if exits, would be ineffective and short

lived.

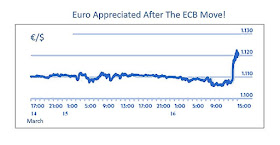

This is evident from the ECB’s March

10th policy announcement of an array of new unconventional policies. Mr. Draghi cut the three official interest

rates; increased the volume of asset

purchases; offered more generous terms on targeted longer-term refinancing

operations, and introduced a liquidity facility for banks pegged to the quantity

of loans on their balance sheet. Given the ineffectiveness of these measures, the only motive that may be detected for their introduction is a hope for a further depreciation of euro. However, this tactical move in the current currency wars, backfired, as it has been the case for Japan. Both currencies appreciated instead of depreciating.

Being oblivious to the longer-term damaging impacts of

negative interest rates on the financial sector, and their distortionary impacts on intertemporal

preferences, ECB reduced euro area deposit rate further down

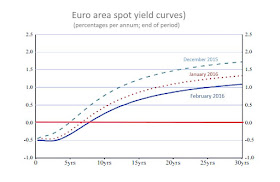

into the negative zone (from -0.3 to -0.4) per cent. As the chart below shows, it is hard to believe that

this move will have any real impact on growth, or will cause a change in the

provision of liquidity. The only impact would be on the expected slope of the

yield curve of up to ten-year maturity, which now is expected to remain relatively flat for a longer

period, exerting more damage to the already fragile banks’ balance sheet.

A flat yield curve removes the banks’ maturity

transformation opportunities. A bank’s ability

of intermediation in the credit market, to transform short-term savings

into long-term loans, is critically compromised by the flat slope of the yield curve. Thus, banks’ profitability is now seriously

impaired. Long term rates are low because markets are anticipating a hard

landing is inevitable.

In terms of helping the global economy the US Federal

Reserves’ policy action on March 16th was not much different. Ms. Yellen markedly revised the pace at

which her bank expects to lift interest rates, justifying the revision by

referring to global worries that could adversely impact America’s recovery.

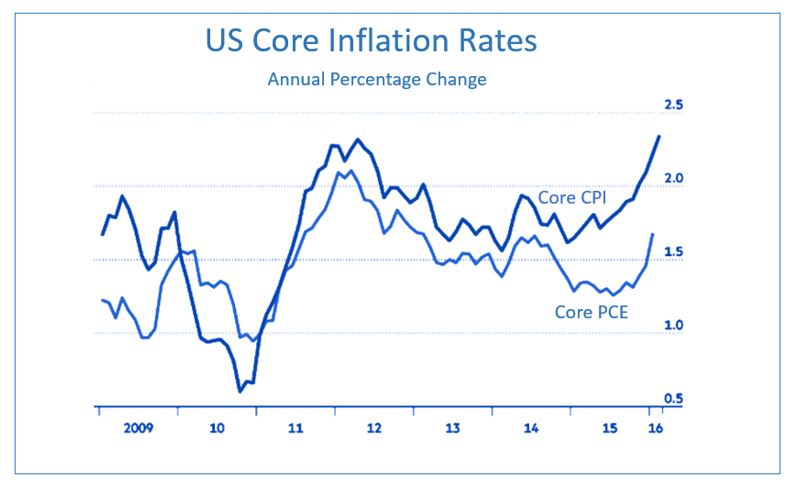

This was despite the fact that core inflation in the US, excluding the

deflationary impact of lower oil prices, has now ticked up to 2.3 per cent,

which is above target for headline inflation of 2 per cent. Ms. Yellen has halved the number of rate

increases that are expected for 2016 to two 25 basis points moves.

However, given our argument with regard to economy’s greater

use of intensive margin, the inflation scenario is now much more complicated. The use

of intensive margin indicates a lower growth of the aggregate potential output,

as investment for extensive margin is being delayed or abandoned. This would

imply a lower non-accelerating inflationary rate of unemployment (NIRU). A lower potential growth rate determined by

an aggregate short-term cost function would cause inflation rate to pulsate in accordance

with the on-off use of contingent factors of production. The impact of these bouts

of inflation rate on the expected inflation could become a potent source of

stagflation.

It is certainly true that the US is now worryingly more

exposed to the global volatility. The alleged surprise of those that consider the Fed’s mandate

is to worry about the US inflation and unemployment, or that did not expect a greater Fed's sensitivity to the worldwide

repercussions of US monetary policy decisions, is at best disingenuous. It is hard to believe that Fed is not using a

structural model in which some forms of covered or uncovered interest rate

parity relationships play an important role in determining the value of the US dollar

against other currencies. In other words, global events would impact the Fed’s policy rate setting via this channel, and then reverberate through the balance of trade. As

soon as one uses a structural model with some interest parity conditions the sensitivity to global impacts would be a foregone conclusion.

Of course, Fed must be acutely aware that all over the world

there are now over $7 trillion worth of bonds with negative yields. In other

words both governments and banks are now being paid to borrow from the various

central banks in the euro area, Japan, Sweden, Denmark, and Suisse. This would elevate the already unsustainable

level

of global debt. A hard landing is becoming even more devastating and painful, when banks are now more vulnerable, more exposed, and larger.

No comments:

Post a Comment