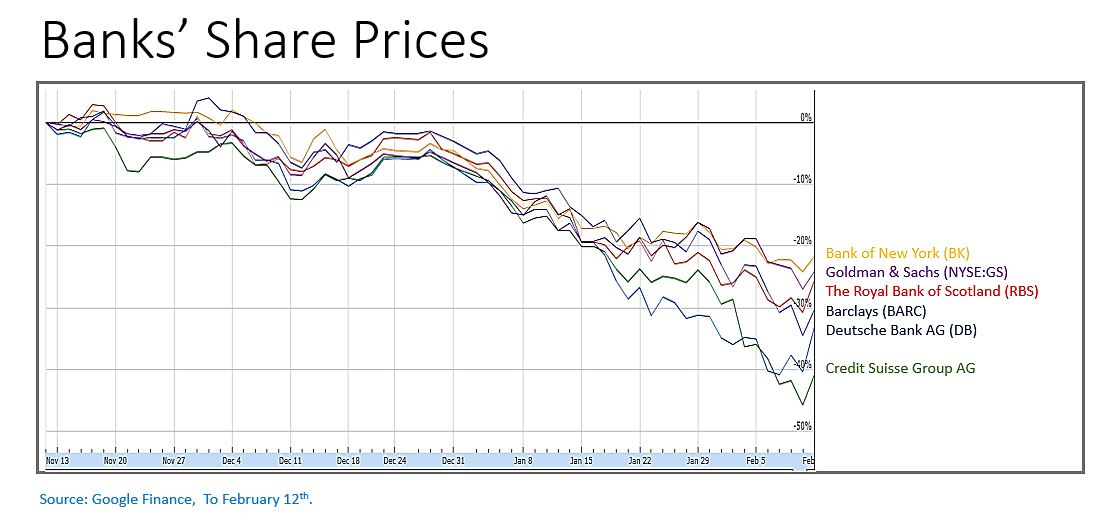

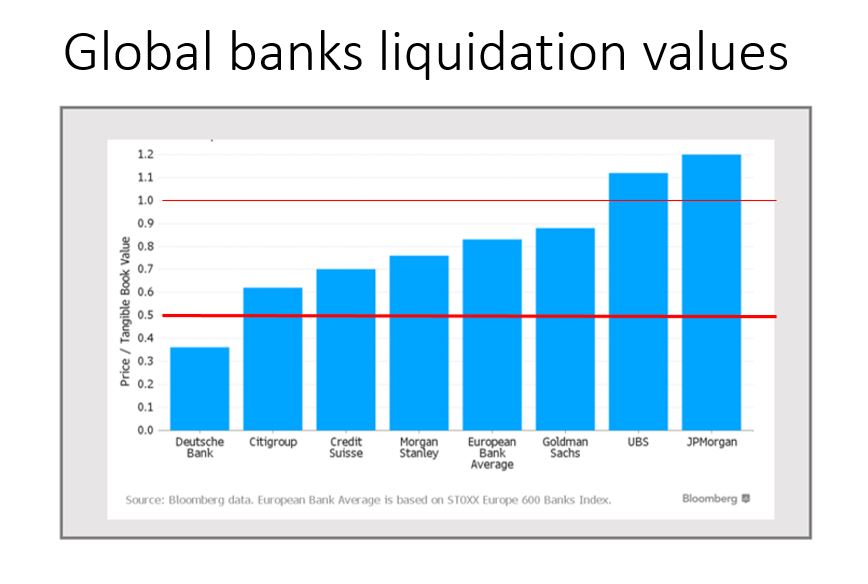

The global financial imbalances have pushed the banking sector off the cliff edge. On February 11th after yet another volatile day in stock markets, bank stocks crushed amid a selloff that has erased more than $4 trillion from global equities this year -- another Minsky Moment is almost upon us. The global distress embraced industry's titans such as Goldman Sachs, Morgan Stanley, Société Générale, Deutsche Bank, Barclays and Credit Suisse among others. Shares of Goldman Sachs and Morgan Stanley, the two American equity-trading giants, dropped by close to 10% below their tangible book value, a theoretical gauge of how much of their worth they could salvage if liquidated.

American financial stocks are down by 19%. French and German banks like Société Générale and Deutsche Bank saw their shares fall by more than 10%, while Italian banks shares have plunged by 31% and those of Greek by an alarming 60%. The European banking shares have lost around 27 percent so far this year. The index of major banking shares in the UK at one point hit its lowest levels since the depths of the recession. Asian banks were also afflicted, for instance Japanese banks’ shares have dropped by 36% this year. The readers of this blog may recall that this outcome were consistently warned against in this forum. Indeed, in July 2015 we wrote:

While $107 billion dollar Greek debt to European banking sector appears manageable, even a rather modest money multiplier inflate that amount to a quite frightening level. In fact, since the inception of the euro in 2001, the German, French, and Dutch banks bought a huge amount of Greek, Portuguese, Spanish and Italian sovereign debts by leveraging their equity capital—this was European version of the US subprime mortgage fiasco. Thus, the balance sheets of these banks, levered up in some cases by forty to one or more, is in a very fragile state. The stability of the system has only been maintained by a rather artificial prolonged surge in global financial markets since 2013, emanating from an extraordinary loose monetary policies in advanced economies. In the words of a December 2014 BIS report, “ample monetary stimulus fueled investors' risk appetite and boosted a search for higher-yielding assets”.We are witnessing another financial contagion, where initial deterioration in banks’ balance sheet resulting from a number of adverse shocks such as the oil market predicaments, China's slowdown, and currency wars are rapidly spreading and the risk quality of financial sector’s loans is plunging into a dark abyss. While market anxieties, reflected in increased intra-euro area spreads and higher term premia, were appearing somewhat abated by ECBs policies; it is now clear that its unconventional monetary policies are ineffective and incapable of correcting the fundamental fragilities.

The risk of low market liquidity has reappeared again with a vengeance. Confidence among large banks with respect to their ability to make markets must be collapsing. ECB like a number of other central banks had hoped that its asset purchase program would eventually support nominal growth and as a result banks’ profitability would be improving. It was assumed that by a simulated shrinkage of banks’ balance sheets and some regulatory improvements in various capital and leverage ratios the lingering post-Big-Recession challenges would be behind us.

However, as the above chart demonstrates shares in institutions from Goldman Sachs to Deutsche Bank have endured a serious slide. Central banks may be able to discount the fact that, as shown by Reinhart and Rogoff, at least in the United States, the ex post probability of being in a financial crisis era has been about 13 percent of the time since the country’s independence – i.e., once about every 8 years. However, they cannot deny that the recent intensification of banking stress as net interest margins are being disappeared under the low interest rate environment and flattening yield curves, has created a severe systemic risk. It is quite clear that the legacy of sovereign debt crisis is still haunting and stock of non-performing loans are on the rise proceeding from the plight of the oil and related services sectors, as well as the expected poor performance of companies that are adversely affected by the slowdown in China, or those that have invested heavily on luxury London real estates which hedge funds are beginning to short.

For much of the last few years various central banks have been performing an extensive set of “stress testing” their balance sheets against a chain of purportedly worst-case economic scenarios, in order to identify which banks do not have sufficient capital to meet the hypothetical shocks, gauging the amount of recapitalisation the banks require. However, policy makers are well aware that no bank can survive these tests when confidence in the banking system has been shattered. As well, nobody knows how the structural parameters of the underlying models for these tests have changed in response to unconventional policies such as negative interest rates. In other words the results of these tests are at best unreliable. The same can be said of calculations that, for instance, show European banks are holding €700m worth of capital more than they were at the time of the last crisis and have disposed of their riskiest assets. These would be misleading if there is a crisis of cofience. Banks’ financial strength is under a question mark and the probabilities of large banks reporting large losses are not trivial.

The crisis is not just concentrated on the banking sector, negative and very low interest rates are overturning the financial business models of pension funds and insurance companies that must constantly struggle to immunize their long-term liabilities (retirement, long-term disability, nursing home or other long-term care). They do this by financing at a comparable investment horizon with a sufficient yield, so that there would be no interest mismatch or duration conflict. However, now more than US$7 trillion in government bonds (mostly from Europe and Japan) comes with negative yield, which have caused something of an existential crisis in the global life insurance industry. European regulators have warned that some major insurers may have to be bailed out if the crisis continues, where payout yields continue to outstrip returns in sovereign bonds.

In the coming weeks we are going to witness more debilitating shocks from the emerging markets, including Saudi Arabia, Venezuela, Turkey, and Brazil. Italian and Greek banks are still fragile. The National Bank of Greece is down 94% this year. In just six weeks, this share has lost almost all of its market value. For many insolvency is just around the corner owing to low oil prices and policy extravaganza. The banking system is in dire need of recapitalization but it is not clear how can this be done? The new "bail-in" rules in Europe mean that senior bondholders and depositors with balances above the guarantee of €100,000 will have to help pay for it, which adds to stress. Of course, North American, and Asian countries will also contribute to various adverse shocks, as the global imbalances and risky balance sheets are interlinked and ubiquitous.

In these circumstances, Italy’s high level of non-performing loans is particularly troubling. Apologists argue that if Italy’s recovery can be sustained they should eventually start to come down, but this is a big if. The fact that over half of the riskiest loans of the country out of €200 billion are covered by special provisions is not particularly helpful. The “bailed in” rules, which have become fully operative for many European countries this year, can trigger a new wave of bankruptcies. As a sign of this many faceted domino effect, it is of note that Goldman Sachs and JP Morgan are now faced with large stakes in Italian oil services company Saipem following their completion of a €3.5 bn (£2.7 bn) share issue with prices that have been falling precipitously.

The prospect that central banks in Europe and Japan will delve even lower into negative rate territory, and the likelihood that Federal Reserve abandoning its move to normalization are creating further uncertainty and contributing to a more volatile market. It is mind bugling that until now none of the US presidential candidates in the both parties’ presidential debates have not shown even a remote interest on discussing this ominous conditions. Meanwhile, European finance ministers who will meet at the end of February in Shanghai in China have decided to call on the Group of 20 biggest world economies to boost global economic growth. They still do not realize that the culprit is a broken financial structure and as Japan experience has demonstrated no amount of infrastructural investment by itself can create growth.

As we have argued before this crisis is aggravated by global illiquidity arising from sever distortion of credit markets and its incapacitating impacts on supply of bank credit. This illiquidity cannot be expunged unless and until a drastic global restructuring of the enormous global debt overhang is underway. In other words, a comprehensive global strategy is urgently needed which must encompass necessarily a readjustment in valuation of foreign exchange rates based on their purchasing power parity. Furthermore, a drastic overhaul of the operational environment is needed to stop the smothering effects of arbitrarily created rules and regulations that are creating distortionary arbitrage opportunities, moral hazards and adverse selection problems. In this respect, the so-called idiosyncratic tailored approaches would be the most perilous strategy, as no agency can claim to have an in-depth grasp of the various dimensions of the current global imbalances.

What is truly needed is a set of clear principle-based rules that would allow the market mechanisms to do their critical functions of price discovery and determine the efficient allocation of resources. The most important market principle in this approach is the resolution of the Too-Big-to-Fail. TBTF problem. However, a reintroducing of Glass-Steagall separations of businesses without other fundamental restructuring would only exacerbate the impacts of distortions. The main concern is not that banks may lose market share. As, undoubtedly, the “shadow banking” environment is also being affected by the scarcity of liquidity and will be contributing to the severity of the ongoing financial crisis. Other purported policy options such as various macroprudential regulations, “the swap push out rule”, “ring fence” banking activity, and “Volcker rule”, that are supposed to limit or ban TBTF firms’ are also inappropriate in the absence of a comprehensive structural overhaul of the system.

No comments:

Post a Comment